In a sliding market, TaskUs has defied the odds, trading up to $16.68 per share. Its 12.6% gain since November 2024 has outpaced the S&P 500’s 2.1% drop. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in TaskUs, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is TaskUs Not Exciting?

We’re glad investors have benefited from the price increase, but we're swiping left on TaskUs for now. Here are three reasons why we avoid TASK and a stock we'd rather own.

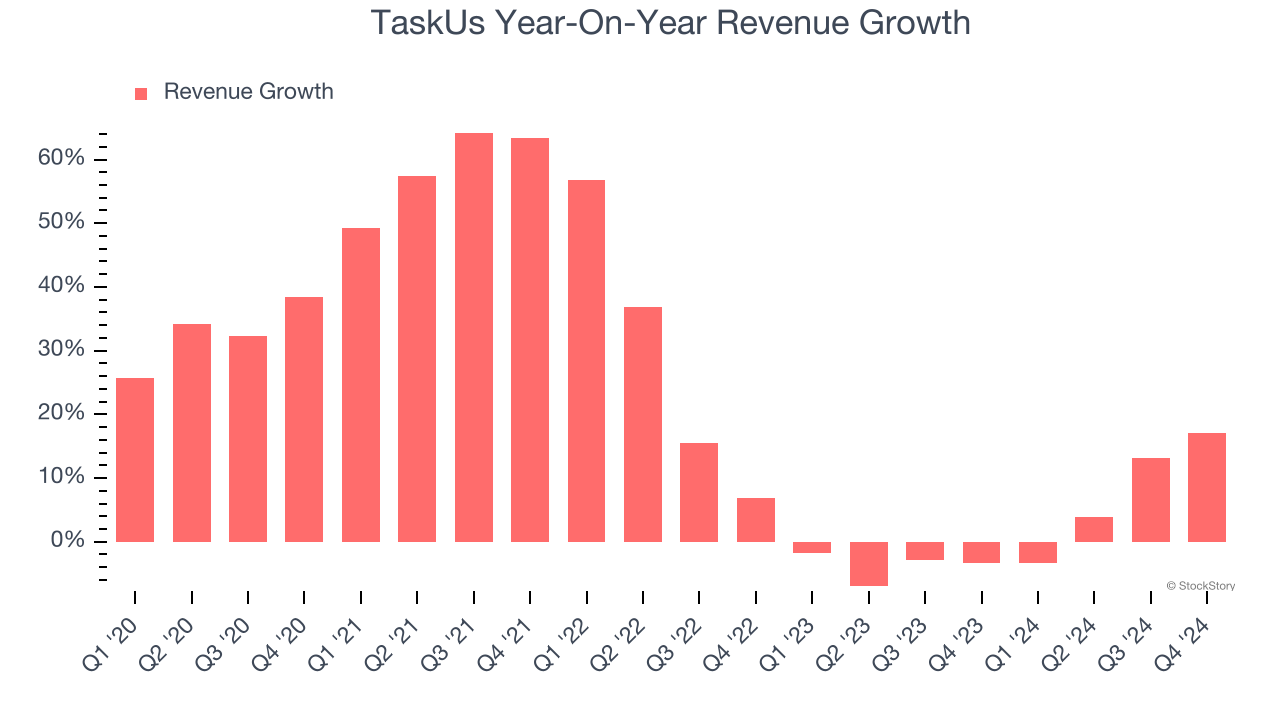

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. TaskUs’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 1.8% over the last two years was well below its five-year trend.

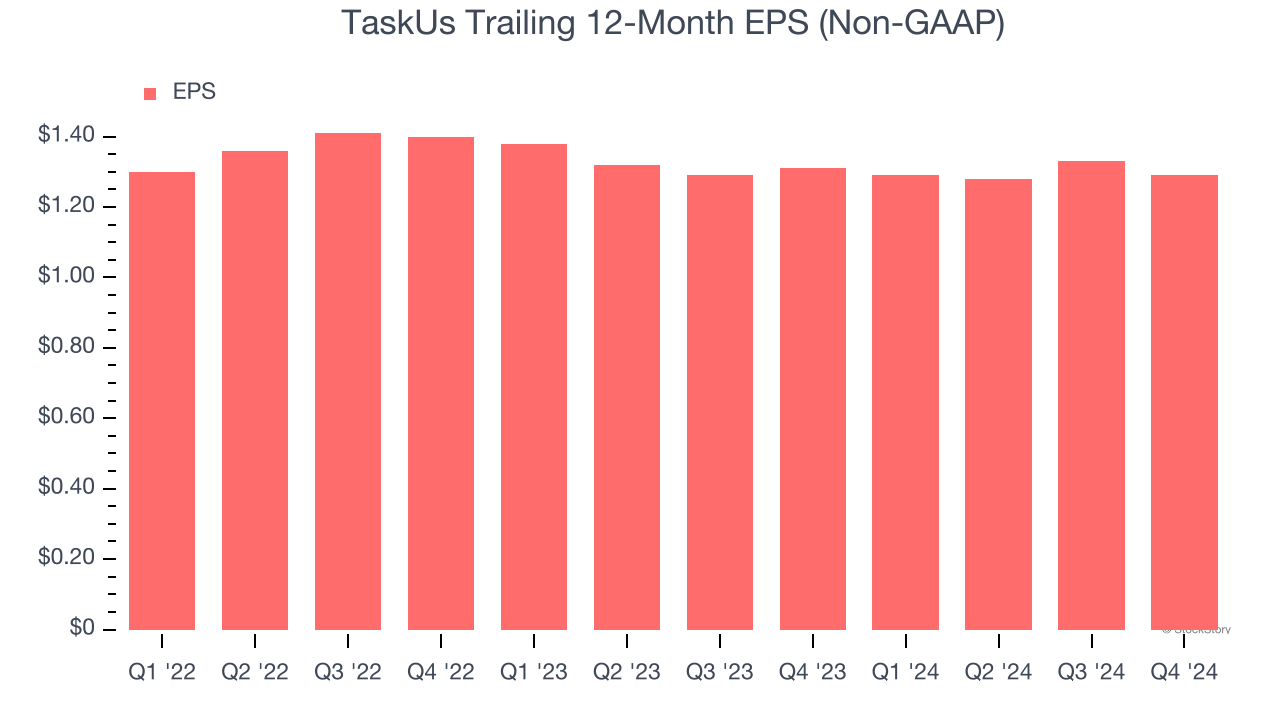

2. EPS Barely Growing

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

TaskUs’s full-year EPS grew at a weak 1% compounded annual growth rate over the last three years, worse than the broader business services sector.

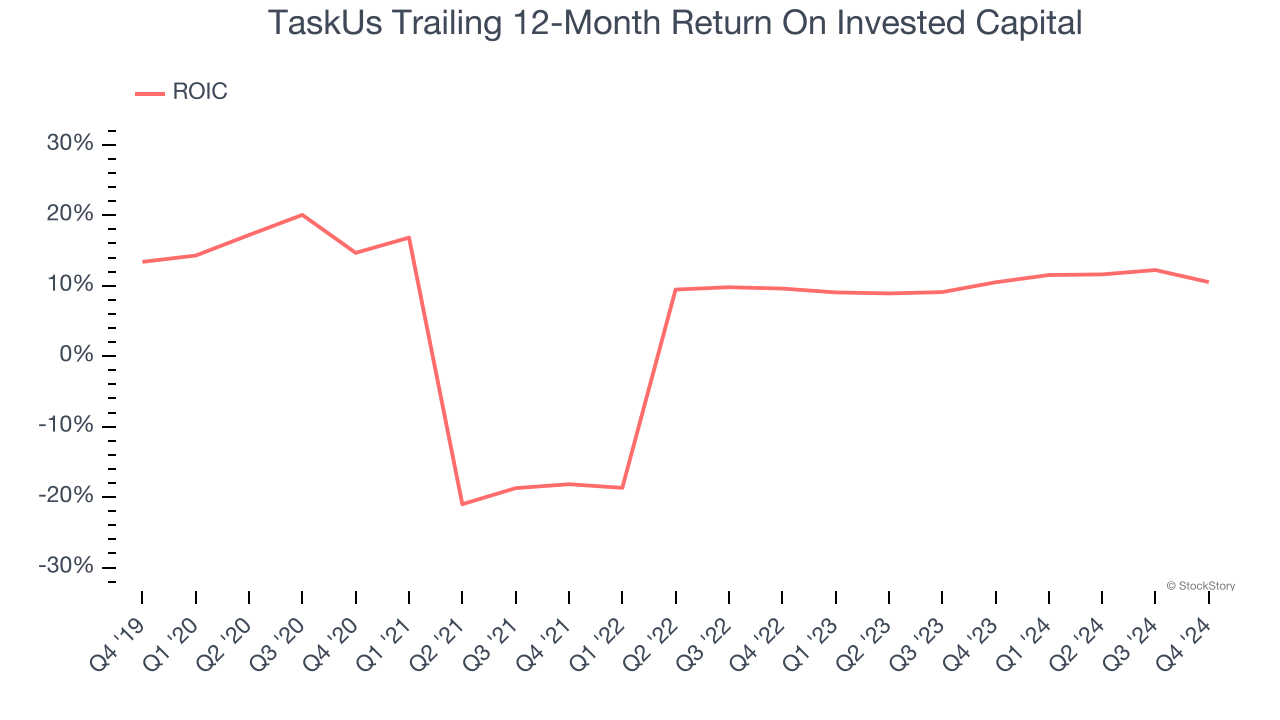

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

TaskUs historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.4%, somewhat low compared to the best business services companies that consistently pump out 25%+.

Final Judgment

TaskUs isn’t a terrible business, but it isn’t one of our picks. With its shares outperforming the market lately, the stock trades at 12.1× forward P/E (or $16.68 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

Stocks We Would Buy Instead of TaskUs

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.