Shareholders of Herc would probably like to forget the past six months even happened. The stock dropped 44.2% and now trades at $124.41. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Herc, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Herc Not Exciting?

Even with the cheaper entry price, we're swiping left on Herc for now. Here are three reasons why we avoid HRI and a stock we'd rather own.

1. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Herc’s revenue to rise by 2.2%, a deceleration versus its 11.6% annualized growth for the past two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

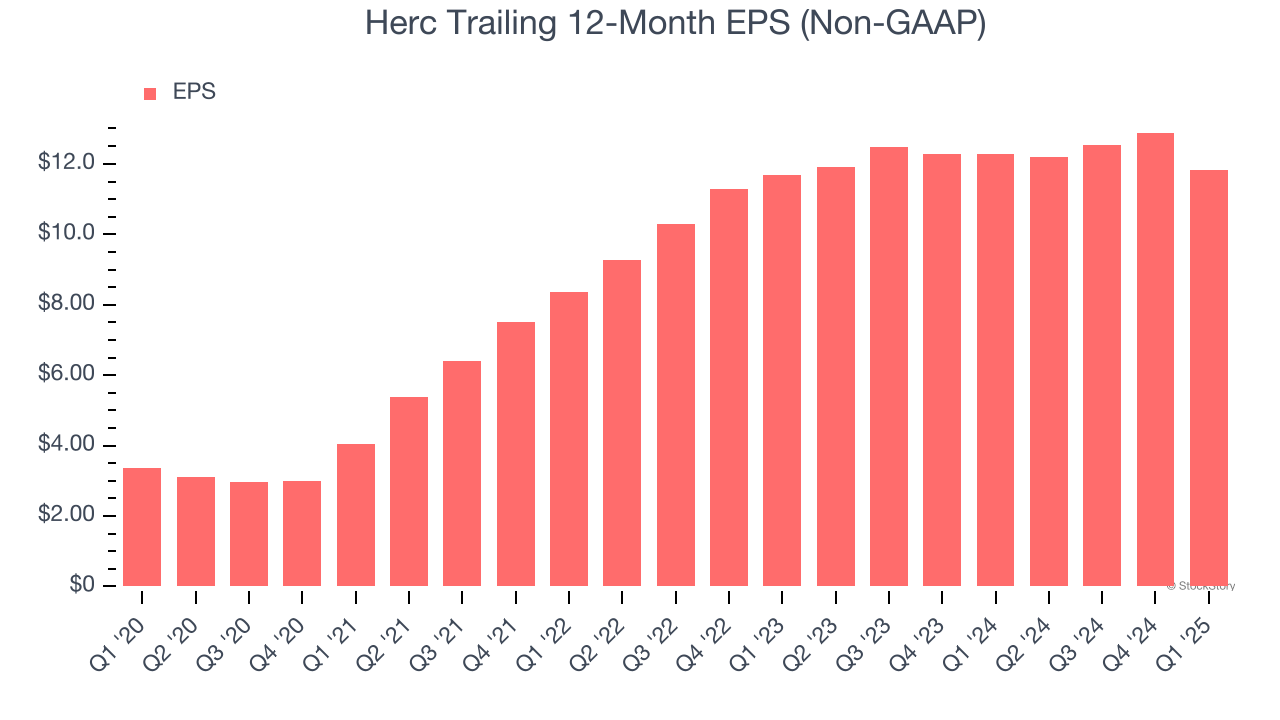

2. EPS Growth Has Stalled Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Herc’s flat EPS over the last two years was worse than its 11.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

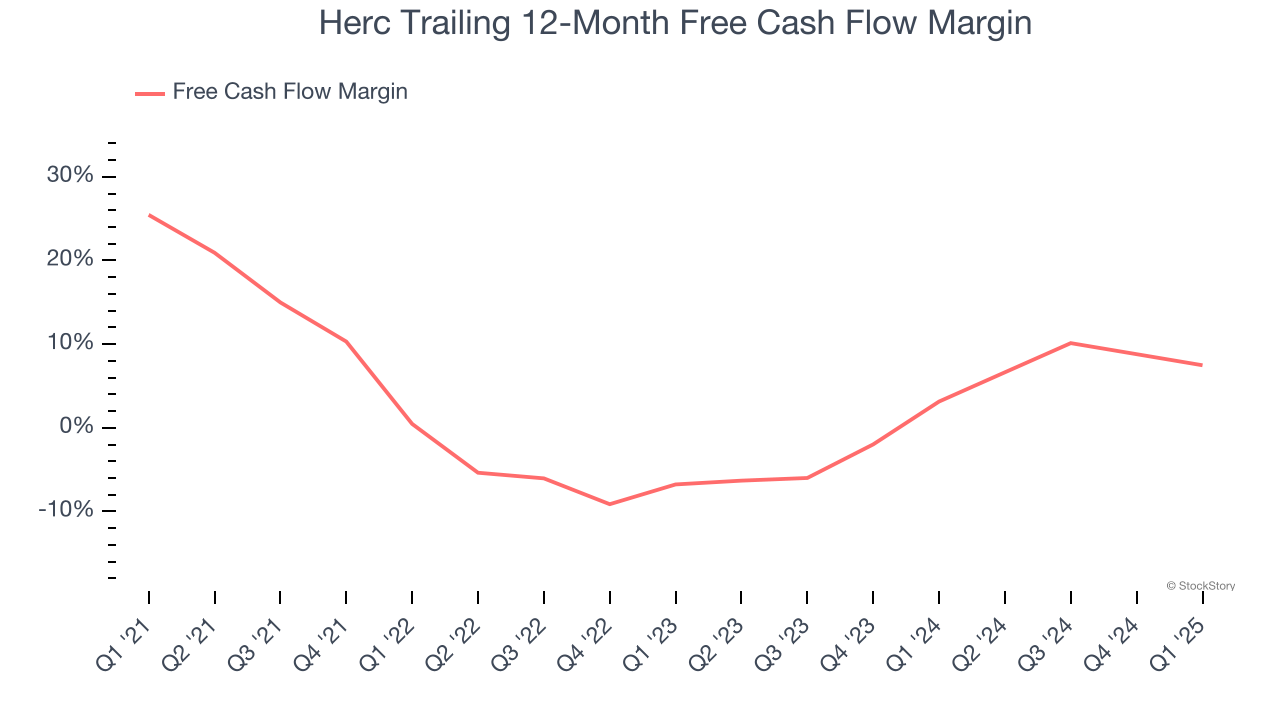

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Herc’s margin dropped by 18 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because of its relatively low cash conversion. If the longer-term trend returns, it could signal it’s becoming a more capital-intensive business. Herc’s free cash flow margin for the trailing 12 months was 7.5%.

Final Judgment

Herc isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 9.7× forward P/E (or $124.41 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now. We’d recommend looking at one of our top digital advertising picks.

Stocks We Like More Than Herc

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.