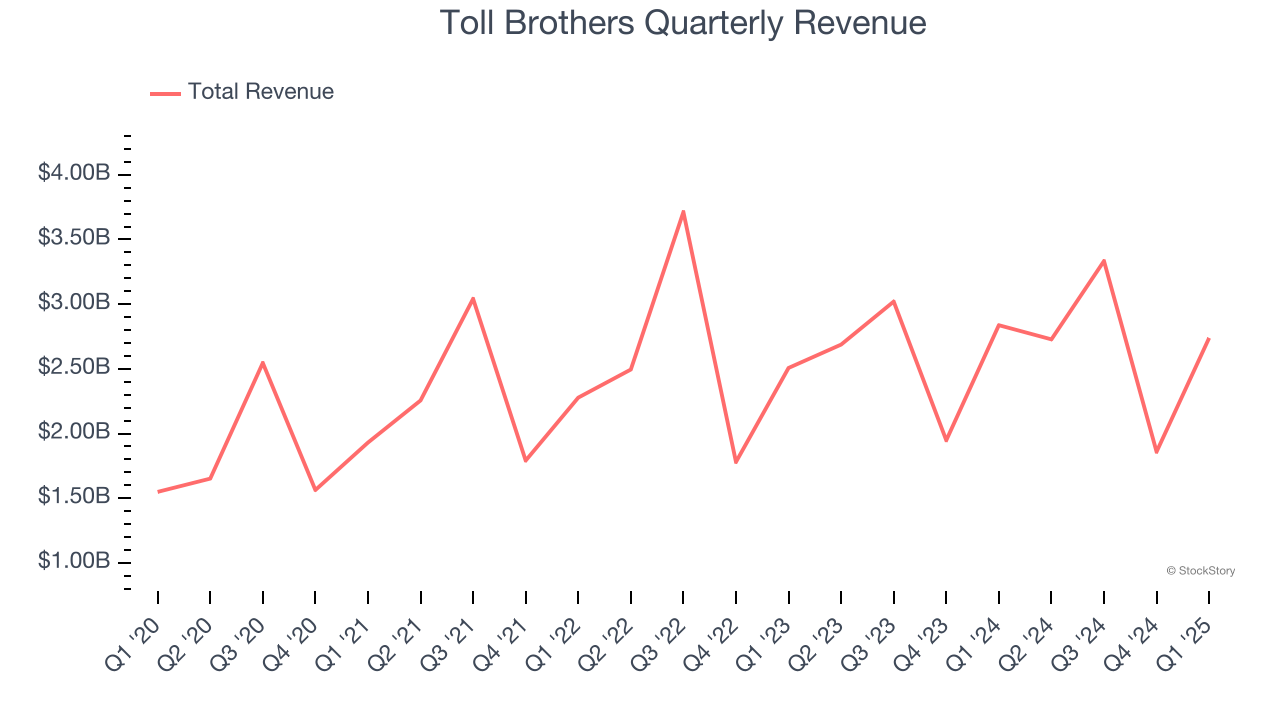

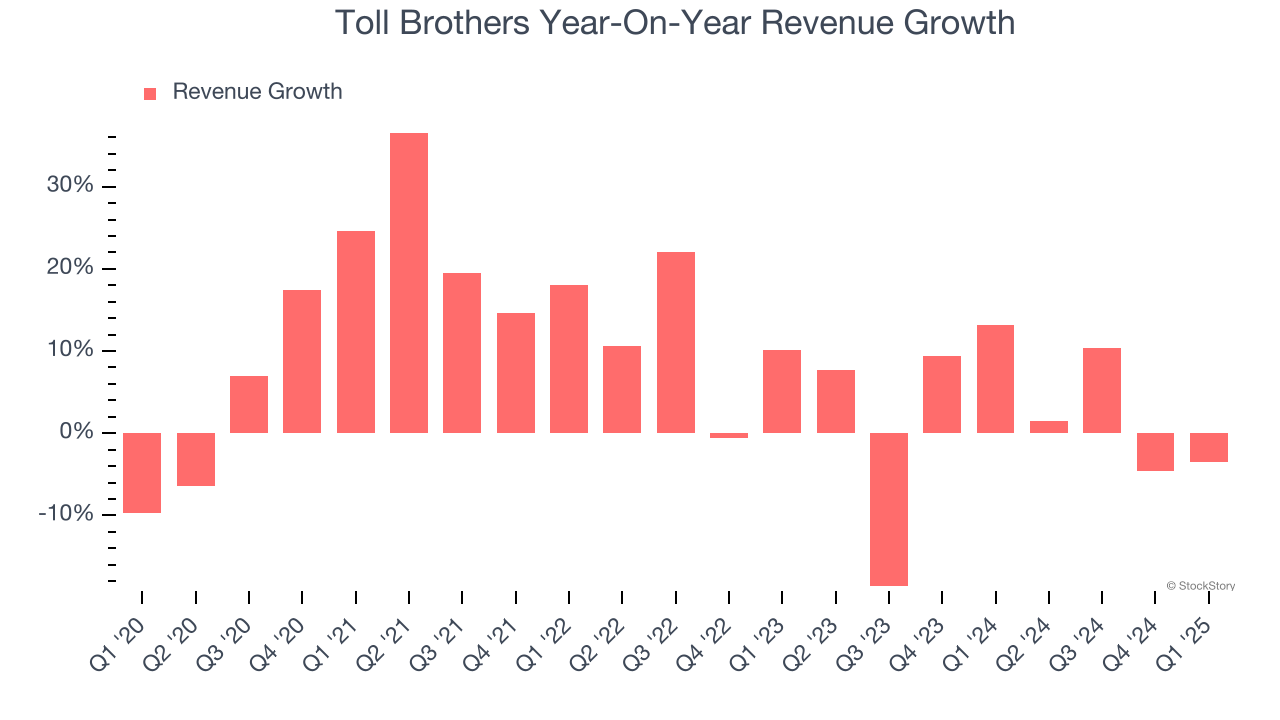

Homebuilding company Toll Brothers (NYSE:TOL) announced better-than-expected revenue in Q1 CY2025, but sales fell by 3.5% year on year to $2.74 billion. Its non-GAAP profit of $3.50 per share was 22.4% above analysts’ consensus estimates.

Is now the time to buy Toll Brothers? Find out by accessing our full research report, it’s free.

Toll Brothers (TOL) Q1 CY2025 Highlights:

- Revenue: $2.74 billion vs analyst estimates of $2.49 billion (3.5% year-on-year decline, 9.9% beat)

- Adjusted EPS: $3.50 vs analyst estimates of $2.86 (22.4% beat)

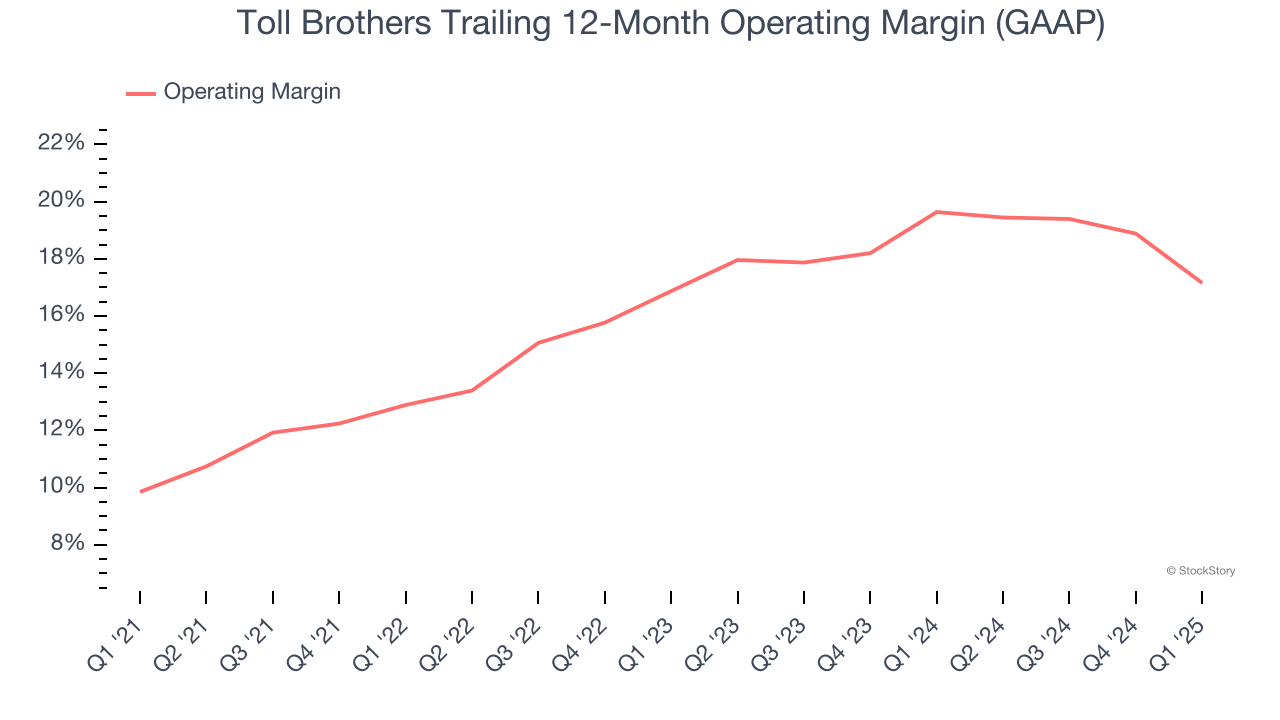

- Operating Margin: 16.4%, down from 23% in the same quarter last year

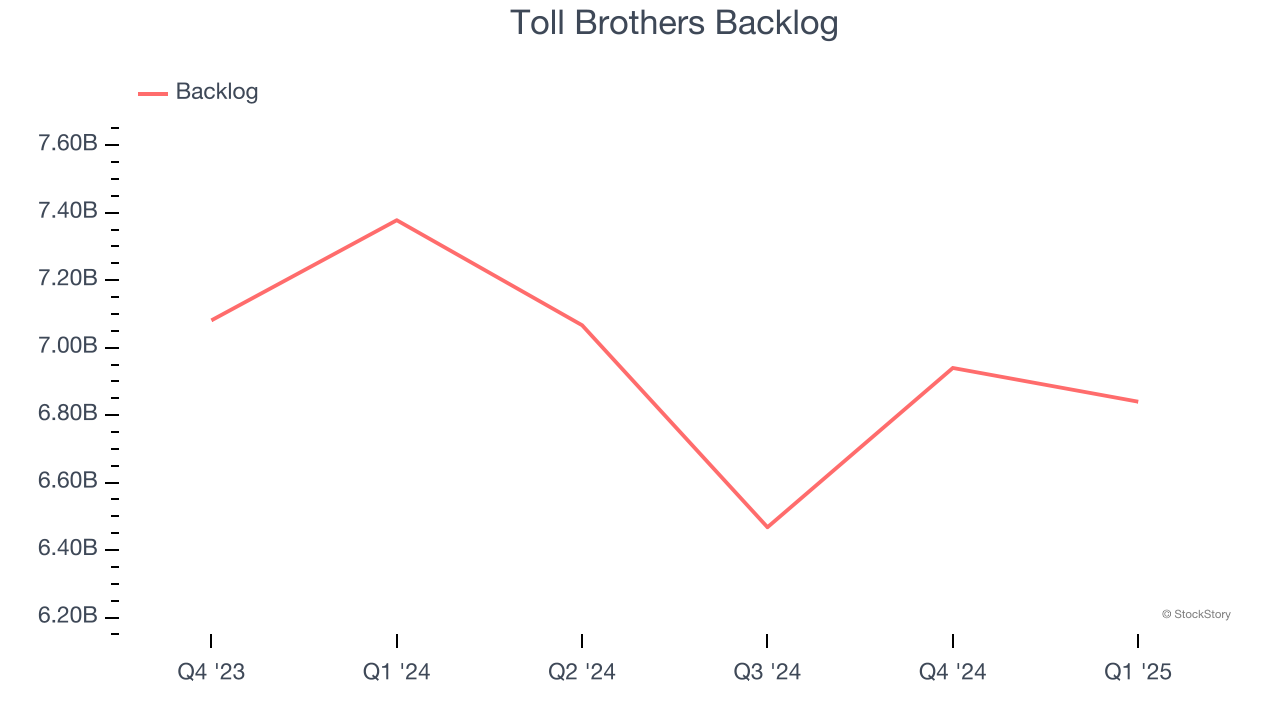

- Backlog: $6.84 billion at quarter end, down 7.3% year on year

- Market Capitalization: $10.55 billion

Douglas C. Yearley, Jr., chairman and Chief Executive Officer, stated: “We are pleased with our second quarter results, as we delivered earnings that significantly exceeded expectations. Despite a softer demand environment, we generated record second quarter home sales revenues of $2.71 billion, well above our guidance of $2.47 billion, and beat both our adjusted gross margin and SG&A guidance. We believe these results highlight the strength of our broadly diversified luxury product offerings, price points and geographies, our balanced portfolio of build-to-order and spec homes, and our strategy of prioritizing sales price and margin over pace in the current environment. Based on our first half results and the strength of our backlog, we are reaffirming our full year guidance."

Company Overview

Started by two brothers who started by building and selling just one home in Pennsylvania, today Toll Brothers (NYSE:TOL) is a luxury homebuilder across the United States.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Toll Brothers’s 8.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Toll Brothers’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Toll Brothers’s backlog reached $6.84 billion in the latest quarter and averaged 4.6% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, Toll Brothers’s revenue fell by 3.5% year on year to $2.74 billion but beat Wall Street’s estimates by 9.9%.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months, similar to its two-year rate. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Toll Brothers has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 15.7%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Toll Brothers’s operating margin rose by 7.3 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q1, Toll Brothers generated an operating profit margin of 16.4%, down 6.6 percentage points year on year. Since Toll Brothers’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

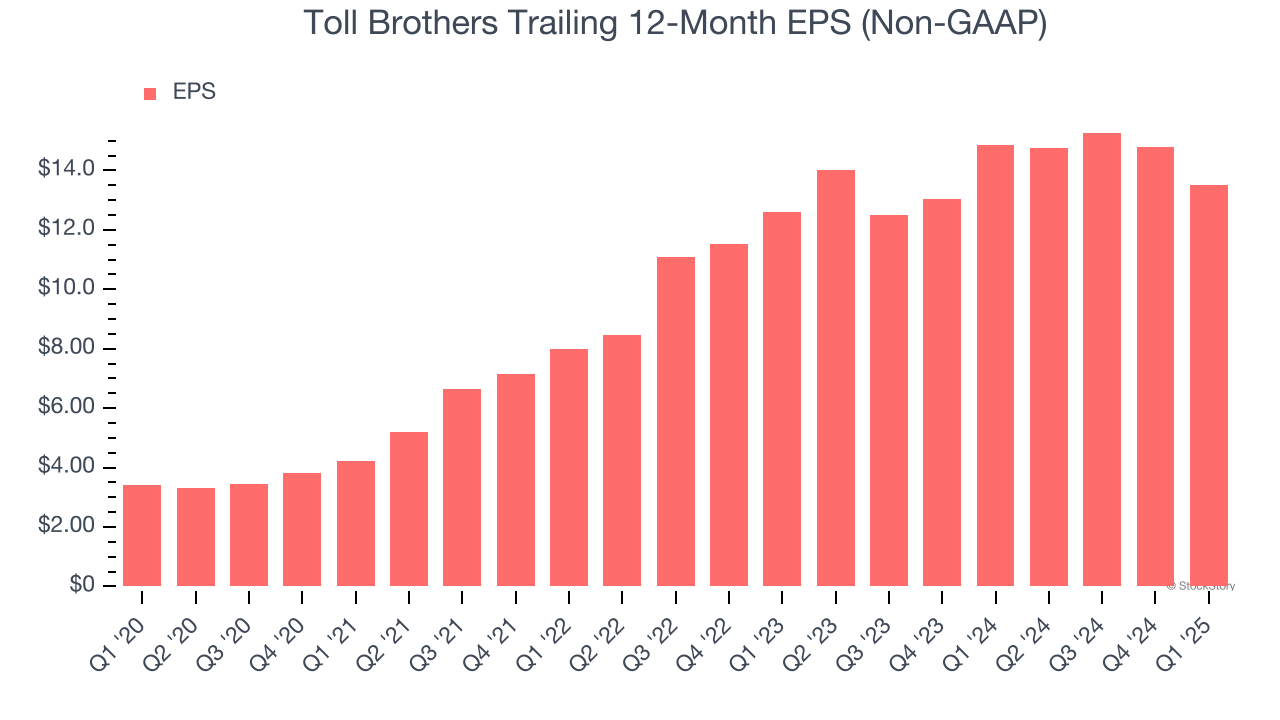

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Toll Brothers’s EPS grew at an astounding 31.7% compounded annual growth rate over the last five years, higher than its 8.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

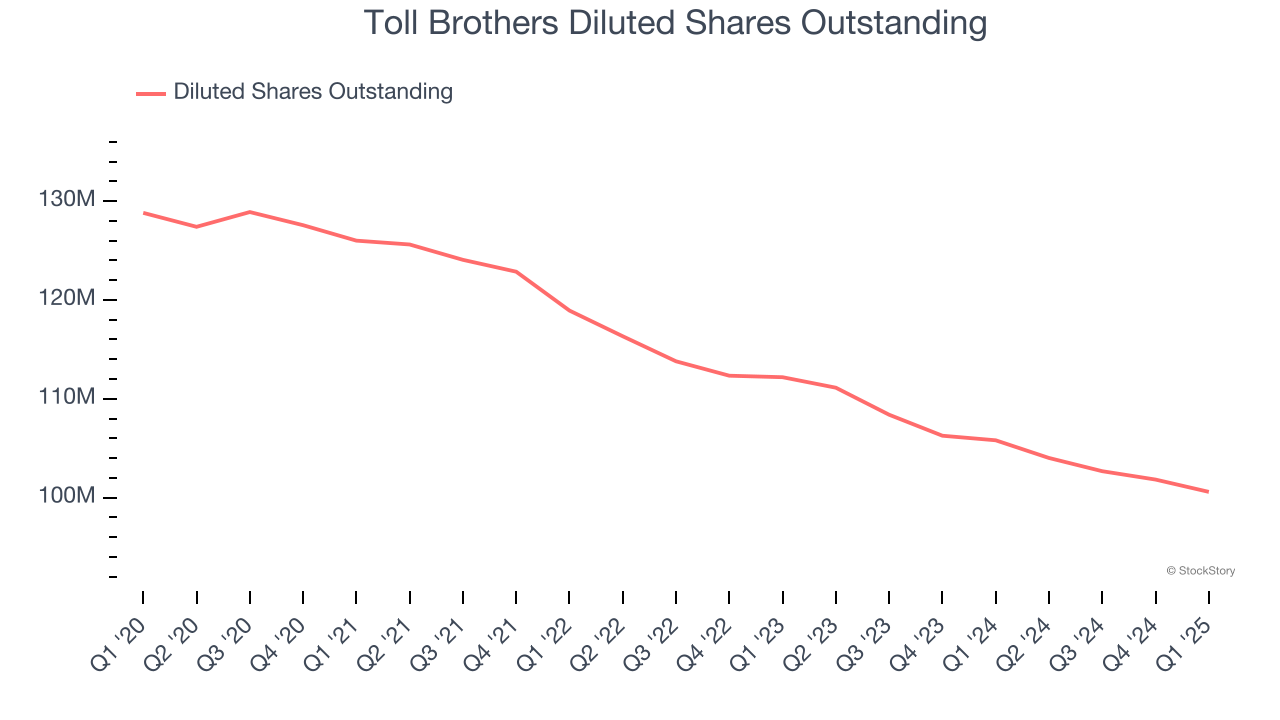

Diving into the nuances of Toll Brothers’s earnings can give us a better understanding of its performance. As we mentioned earlier, Toll Brothers’s operating margin declined this quarter but expanded by 7.3 percentage points over the last five years. Its share count also shrank by 21.9%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Toll Brothers, its two-year annual EPS growth of 3.6% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q1, Toll Brothers reported EPS at $3.50, down from $4.75 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Toll Brothers’s full-year EPS of $13.52 to grow 6.1%.

Key Takeaways from Toll Brothers’s Q1 Results

We were impressed by how significantly Toll Brothers blew past analysts’ revenue and EPS expectations this quarter. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 5% to $109.65 immediately after reporting.

Indeed, Toll Brothers had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.