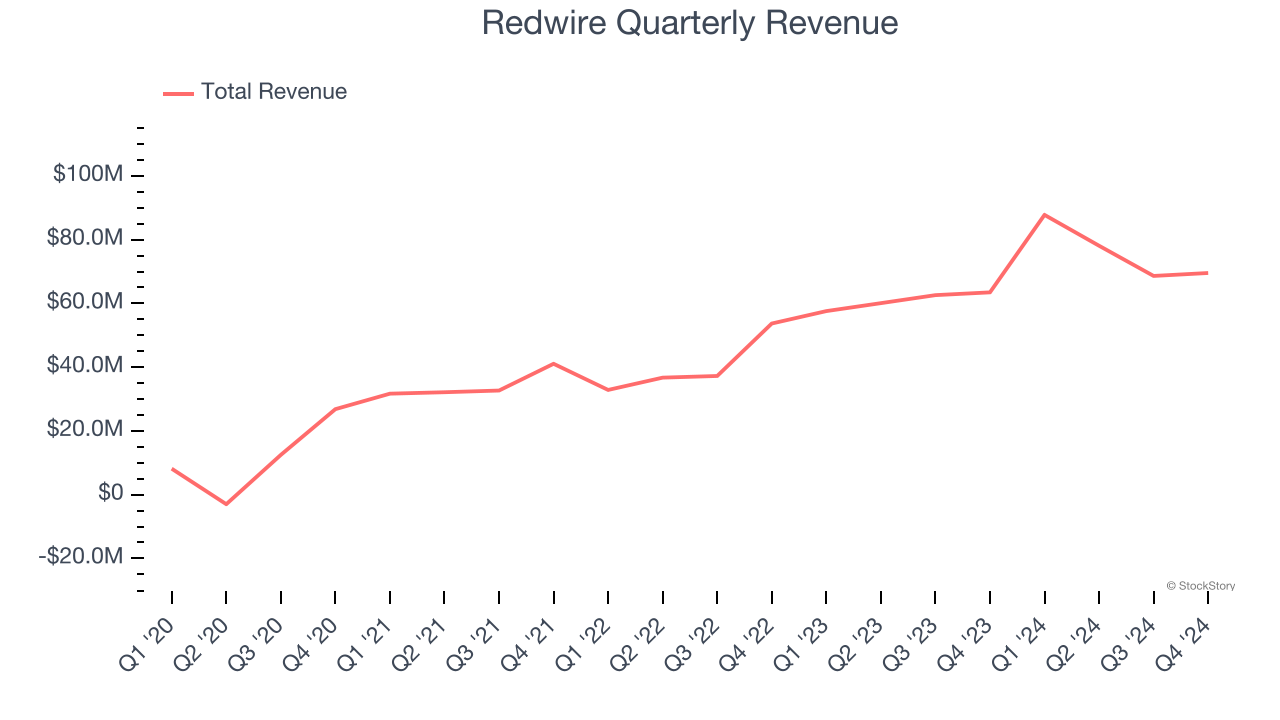

Aerospace and defense company Redwire (NYSE:RDW) fell short of the market’s revenue expectations in Q4 CY2024, but sales rose 9.6% year on year to $69.56 million. On the other hand, the company’s full-year revenue guidance of $570 million at the midpoint came in 24.2% above analysts’ estimates. Its GAAP loss of $1.38 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Redwire? Find out by accessing our full research report, it’s free.

Redwire (RDW) Q4 CY2024 Highlights:

- Revenue: $69.56 million vs analyst estimates of $74.55 million (9.6% year-on-year growth, 6.7% miss)

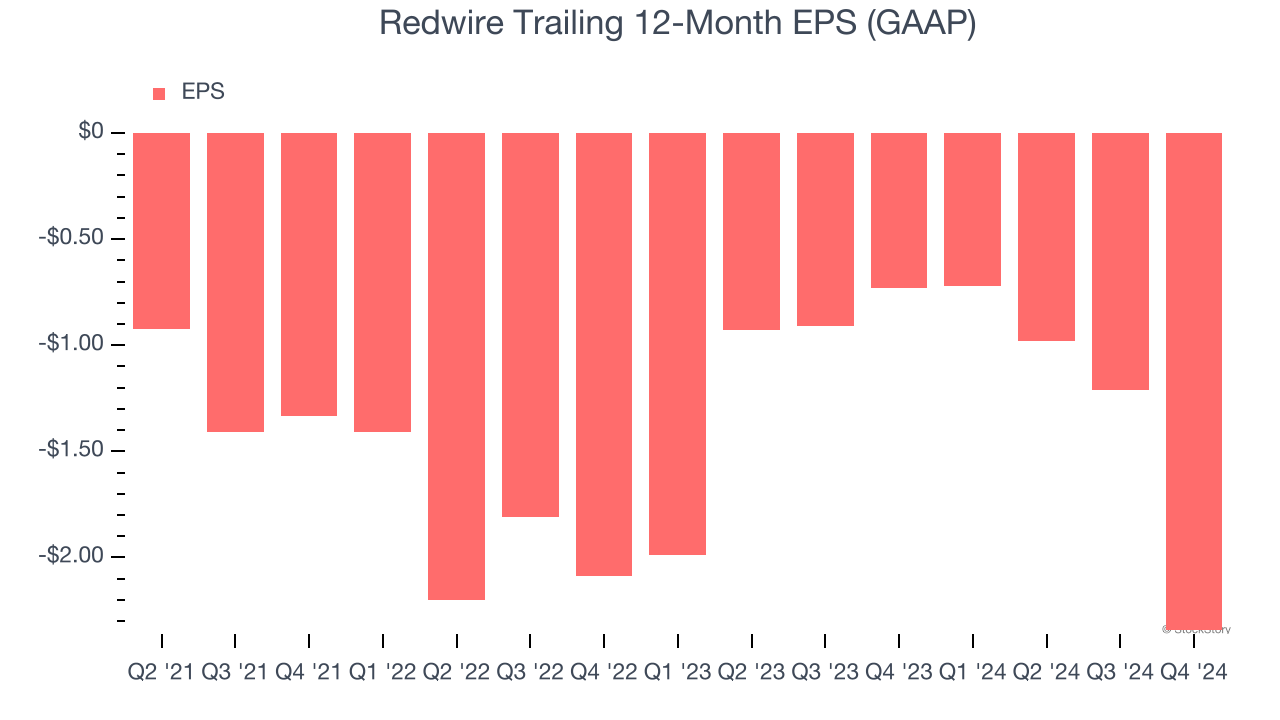

- EPS (GAAP): -$1.38 vs analyst estimates of -$0.18 (significant miss)

- Adjusted EBITDA: -$9.15 million vs analyst estimates of $1.63 million (-13.2% margin, significant miss)

- Management’s revenue guidance for the upcoming financial year 2025 is $570 million at the midpoint, beating analyst estimates by 24.2% and implying 87.4% growth (vs 25.4% in FY2024)

- EBITDA guidance for the upcoming financial year 2025 is $87.5 million at the midpoint, above analyst estimates of $47.45 million

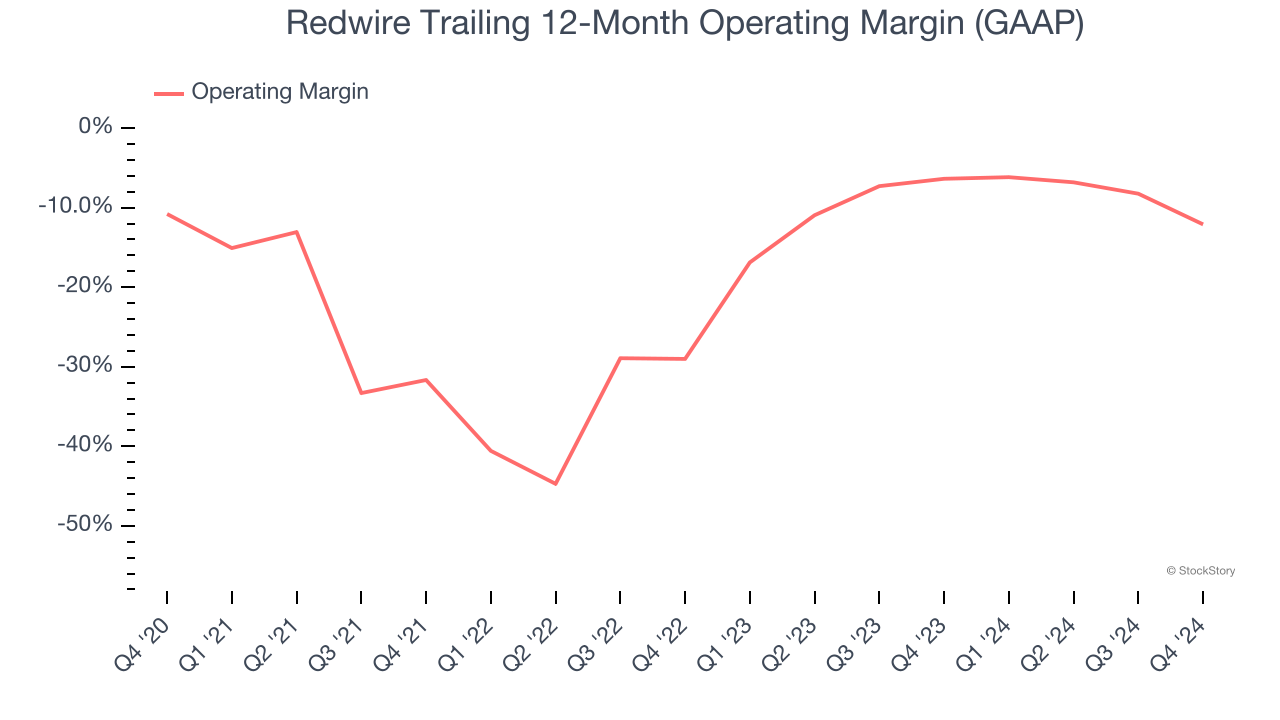

- Operating Margin: -27.3%, down from -10.6% in the same quarter last year

- Free Cash Flow Margin: 4.3%, down from 21.4% in the same quarter last year

- Backlog: $296.7 million at quarter end

- Market Capitalization: $808.2 million

Company Overview

Based in Jacksonville, Florida, Redwire (NYSE:RDW) is a provider of systems and components used in space infrastructure.

Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Sales Growth

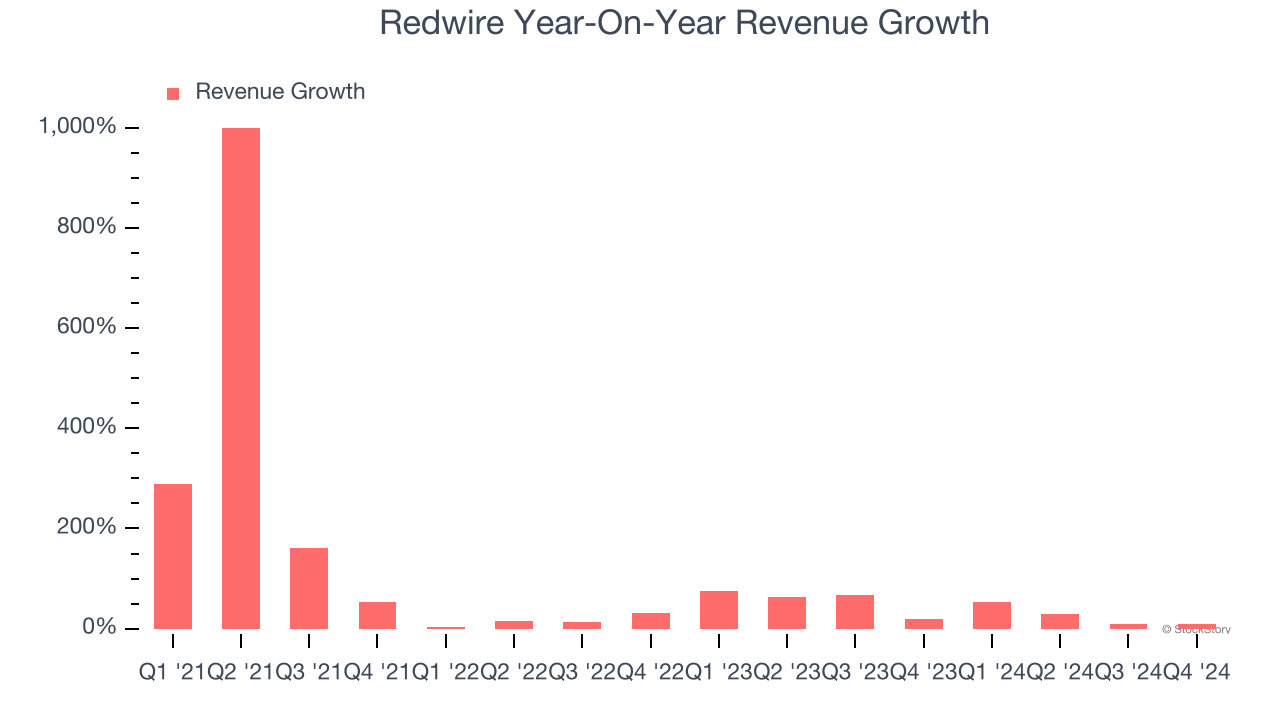

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last four years, Redwire grew its sales at an incredible 61.7% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Redwire’s annualized revenue growth of 37.6% over the last two years is below its four-year trend, but we still think the results were good and suggest demand was healthy.

This quarter, Redwire’s revenue grew by 9.6% year on year to $69.56 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 50.2% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Redwire’s high expenses have contributed to an average operating margin of negative 16.5% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Redwire’s operating margin decreased by 1.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. . Redwire’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

Redwire’s operating margin was negative 27.3% this quarter. The company's consistent lack of profits raise a flag.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Redwire’s earnings losses deepened over the last four years as its EPS dropped 57% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Redwire’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Redwire, its two-year annual EPS declines of 5.8% show it’s still underperforming. These results were bad no matter how you slice the data.

In Q4, Redwire reported EPS at negative $1.38, down from negative $0.25 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Redwire’s full-year EPS of negative $2.34 will reach break even.

Key Takeaways from Redwire’s Q4 Results

We were impressed by Redwire’s optimistic full-year EBITDA guidance, which beat analysts’ expectations. On the other hand, its revenue missed significantly and its EBITDA fell short of Wall Street’s estimates in the quarter. Overall, this was a softer quarter. The stock traded down 19.4% to $9.08 immediately following the results.

Should you buy the stock or not? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.